Health insurance is generally mandatory

People who live or work in the Netherlands usually need Dutch basic health insurance within the applicable official timeline.

Netherlands · Services · Insurance providers

Understand Dutch insurance requirements and compare providers offering health, liability, home, travel and expat-focused insurance products.

Most residents in the Netherlands interact with several forms of insurance. Health insurance is the best-known requirement, but many households also compare liability insurance, home insurance, contents insurance, travel insurance and, for entrepreneurs, business insurance.

Some insurance types are mandatory while others are optional but common. This guide explains the major categories, shows real providers to compare and links you into healthcare, housing, business and relocation content so you can keep researching without treating this page as personal advice.

Insurance products, premiums, exclusions and acceptance rules can change. Use this page as a high-trust starting point, then verify coverage, terms and prices directly with providers and official sources.

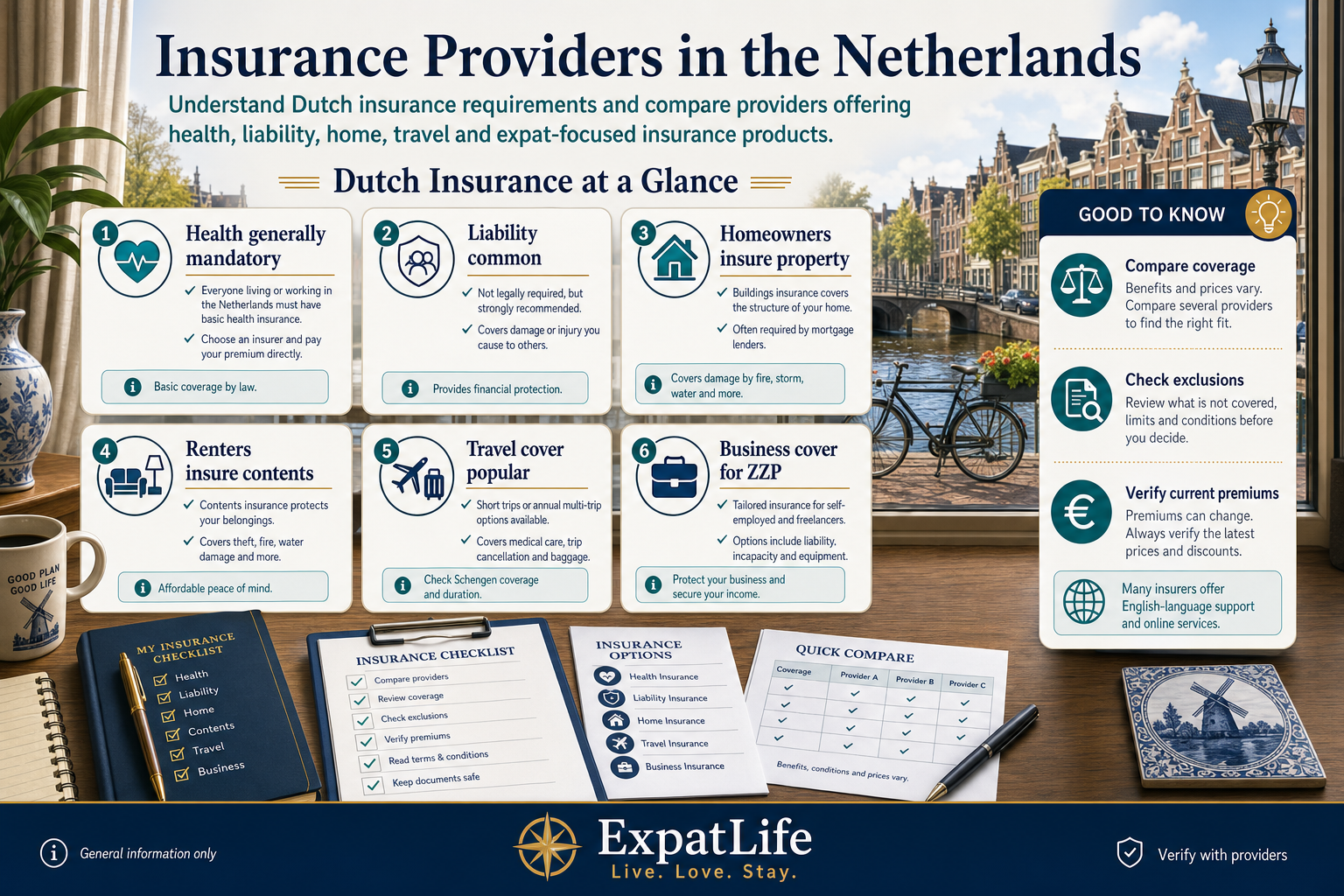

Dutch Insurance at a Glance

People who live or work in the Netherlands usually need Dutch basic health insurance within the applicable official timeline.

Personal liability insurance is not usually mandatory, but many Dutch households choose it for everyday liability risks.

Mortgage lenders and homeowners commonly look at building insurance, contents insurance and related owner risks.

Tenants commonly compare contents insurance for belongings, especially in furnished or temporary expat housing.

Many internationals compare single-trip or continuous travel cover because holidays, home-country visits and business trips are frequent.

ZZP'ers and entrepreneurs may compare professional liability, business liability, equipment and income protection products.

Insurance in the Netherlands is easier to navigate when you separate mandatory products from optional household, travel and business products.

Dutch basic healthcare cover is government-defined and offered by licensed health insurers. Supplementary packages are optional.

May help protect against certain personal liability situations, subject to policy conditions and exclusions.

Usually focused on the building itself and most relevant for homeowners, mortgage borrowers and owner-occupiers.

Covers household belongings under policy conditions and is commonly compared by renters and homeowners.

Can cover trips, baggage, cancellations or medical costs abroad depending on the selected product.

Legal expenses cover may help with certain disputes, but scope and waiting periods vary.

Motor vehicle liability insurance is required if you own and use a car in the Netherlands.

Business liability, professional liability and sector-specific products matter for many entrepreneurs.

Income protection can be relevant for self-employed people who do not have employer sick-pay protection.

Life insurance is often considered alongside mortgages, family planning and long-term financial planning.

Health insurance is one of the most important insurance products for residents. The Dutch basic package is defined by the government, while insurers differ in premiums, policy type, contracted care, digital experience, service model and supplementary packages.

Expats should pay close attention to the start date, residence or work status, whether supplementary coverage is useful and how the insurer handles English-language service. Students, cross-border workers and temporary residents should verify their situation with official sources.

Residents and workers generally need Dutch basic insurance, but students and short-term cases should verify their situation.

Premium, contracted care, reimbursement model and voluntary excess can matter as much as the insurer name.

Dental, physiotherapy and other add-ons are optional. Compare limits and waiting periods before adding extras.

Liability insurance may help protect against certain personal liability situations, such as accidentally causing damage to someone else's property. It is different from health insurance, home insurance and business liability insurance.

Many Dutch residents choose personal liability insurance because premiums can be relatively low and everyday risks are easy to underestimate. Coverage, family members, exclusions and claim limits differ by provider.

Single, partner, family and household definitions can differ, so confirm whether children or housemates are included.

Intentional damage, business activity, vehicles, sports or rented-property situations may be excluded or limited.

Personal liability insurance is not the same as professional or business liability insurance for ZZP work.

Housing status matters. A homeowner, a tenant in a furnished apartment, a family in temporary accommodation and someone buying with a mortgage may all need different insurance conversations.

Before signing, check what the landlord, owners' association, lender or relocation package already covers and what remains your responsibility.

Usually focused on the structure of the home. Most relevant for homeowners and mortgage borrowers; renters normally do not insure the building itself.

Usually focused on belongings inside the home. Relevant for renters, homeowners and expats in furnished or temporary housing.

Homeowners usually think about the building; renters usually start with belongings and liability.

Landlords, owners' associations and mortgage lenders can affect what you need to arrange yourself.

Photos, receipts and a simple inventory can make contents cover easier to compare and use.

Many expats travel frequently for holidays, family visits, remote work, business trips or relocation periods. Travel insurance may cover issues such as trip cancellation, baggage, assistance and some medical costs abroad, depending on the product.

Continuous annual travel insurance can be convenient for frequent travelers, while single-trip cover may suit occasional travel. Always check destination, duration, business-travel use, pre-existing conditions and whether Dutch health insurance already covers part of the situation.

Single-trip cover can fit occasional holidays; continuous cover may suit frequent home-country visits.

Work trips, remote work and conferences may need different wording than holiday travel.

Dutch health insurance, travel cover and destination rules can overlap. Confirm what happens outside the Netherlands.

Entrepreneurs and ZZP'ers often need to think beyond personal insurance. Contracts, clients, industry rules and equipment can all influence which risks should be discussed with an insurer or qualified advisor.

Common categories include professional liability, business liability, equipment insurance and income protection. Some clients may require specific cover before signing a contract.

Client agreements may require professional liability, business liability or proof of cover before work starts.

ZZP'ers often need to think about illness, laptop or tools, and whether work stops if equipment is lost.

Insurance needs can change when you add clients, subcontractors, stock, equipment or new service lines.

Needs vary significantly by individual situation, especially during arrival, temporary housing and international travel periods.

Check the timing for health insurance and whether temporary cover bridges the period before Dutch policies start.

Short leases, employer housing and moving shipments can create gaps between travel, contents and relocation cover.

Confirm whether home-country cover still applies after registration, work start or becoming Dutch resident.

Ask what the landlord, platform or relocation provider covers and what personal belongings remain your responsibility.

Frequent trips may require checking duration limits, business use, countries covered and medical treatment abroad.

Partners, children and housemates may not be covered automatically. Check policy holder and household definitions.

These are real providers and insurance groups expats often encounter while researching Dutch insurance. Inclusion is informational, not a ranking, endorsement or recommendation.

Price notes use public 2026 premiums or example profiles where available. Treat them as orientation only because quotes can change with your address, household, excess, policy type, add-ons and business activity.

Expat-relevant

Large Dutch health insurer often compared for basic and supplementary health insurance, online self-service and broad healthcare-provider network options.

Costs and prices

2026 basic health premiums are EUR 153.95, EUR 159.25 or EUR 176.45 per adult per month at the EUR 385 mandatory excess, depending on the selected policy.

What they offer

Pros

Watch-outs

Expat-relevant

Major Dutch health insurer offering basic and additional health insurance with digital policy management and care-finder tools.

Costs and prices

2026 basic health premiums include EUR 149.90 for Basis Keuze, EUR 154.25 for Ruime Keuze and EUR 171.65 for Eigen Keuze per adult per month at EUR 385 excess.

What they offer

Pros

Watch-outs

Expat-relevant

Large health insurer offering Dutch basic insurance, supplementary packages and online tools for managing policies and care choices.

Costs and prices

2026 basic health premiums are EUR 156.95, EUR 159.99 or EUR 177.50 per adult per month at EUR 385 excess, depending on policy type.

What they offer

Pros

Watch-outs

Expat-relevant

Dutch health insurer with basic and supplementary healthcare products, online account management and care guidance resources.

Costs and prices

2026 basic health premiums are EUR 151.25 for Basis Voordelig, EUR 156.25 for Basis and EUR 175.75 for Basis Vrij per adult per month at EUR 385 excess.

What they offer

Pros

Watch-outs

Expat-relevant

Consumer insurer offering modular online insurance products across health, liability, home, contents, travel and car categories.

Costs and prices

2026 FBTO health premiums are EUR 148.75, EUR 159.25 or EUR 167.95 per adult per month at EUR 385 excess. Market examples show FBTO contents cover can start around EUR 2.44 per month for a specific comparison profile.

What they offer

Pros

Watch-outs

Expat-relevant

Large financial services and insurance provider offering personal, home, travel, income, life and business insurance products.

Costs and prices

Public 2026 travel-insurance examples for Nationale-Nederlanden show roughly EUR 5.74-EUR 7.53 per month for one-person continuous travel cover in sample profiles; home and business premiums require a personal quote.

What they offer

Pros

Watch-outs

Expat-relevant

Dutch insurer offering a broad mix of personal, property, mobility, income and business insurance products through several brands and channels.

Costs and prices

a.s.r. lists contents insurance from EUR 4.16 per month and continuous travel insurance from EUR 3.40 per month. Liability examples are around EUR 2.88 per month for a single-person profile, depending on cover and excess.

What they offer

Pros

Watch-outs

Expat-relevant

Cooperative insurer offering health, personal liability, home, contents, travel, vehicle and business insurance options.

Costs and prices

2026 Univé basic health premiums are EUR 147.40, EUR 149.90, EUR 155.00 or EUR 173.20 per adult per month at EUR 385 excess, depending on selected policy.

What they offer

Pros

Watch-outs

Expat-relevant

Direct insurer offering online policy management across health and several everyday personal insurance categories.

Costs and prices

OHRA's 2026 basic health insurance is EUR 159.55 per adult per month at the EUR 385 excess. Public travel-insurance comparisons show OHRA examples from about EUR 2.53 per month for a specific one-person profile.

What they offer

Pros

Watch-outs

Dutch provider

Independent Dutch health insurer known for health insurance products and annual premium announcements; compare policy details directly.

Costs and prices

DSW's 2026 basic health premium is EUR 158.50 per adult per month. Check DSW's current policy page for the exact excess, voluntary-excess discount and supplementary-package costs.

What they offer

Pros

Watch-outs

Expat-relevant

Dutch insurer offering personal, home, travel, vehicle and business insurance, often accessed through Rabobank channels.

Costs and prices

Interpolis calculates most premiums personally through Rabobank. A public student contents example starts from EUR 1.98 per month; other household and travel products depend on household, cover and bundle choices.

What they offer

Pros

Watch-outs

Expat-relevant

International insurer with Dutch products across travel, mobility, property, liability and business insurance categories.

Costs and prices

Allianz Direct states continuous travel insurance can start around EUR 1.50 per month for a single person and around EUR 3.00 for a family; home and liability premiums are calculated from postcode, household and cover choices.

What they offer

Pros

Watch-outs

Expat-relevant

Global risk and insurance services firm offering business insurance, employee benefits and international insurance support through Dutch operations.

Costs and prices

Aon international student-insurance materials show examples around EUR 15.90-EUR 53.70 per month depending on package and status. Business and employee-benefit pricing is quote-based.

What they offer

Pros

Watch-outs

Use this matrix to identify which providers may be relevant by product category before checking current terms directly.

| Provider | Health Insurance | Home Insurance | Liability Insurance | Travel Insurance | Business Insurance | Online Services |

|---|---|---|---|---|---|---|

| Zilveren Kruis | ||||||

| VGZ | ||||||

| CZ | ||||||

| Menzis | ||||||

| FBTO | ||||||

| Nationale-Nederlanden | ||||||

| a.s.r. | ||||||

| Univé | ||||||

| OHRA | ||||||

| DSW | ||||||

| Interpolis | ||||||

| Allianz | ||||||

| Aon |

Product availability can change and may vary by channel, package or underwriting outcome. Verify directly with each provider.

These are broad orientation ranges only. They are not quotes, guarantees or advice.

Health insurance

About EUR 130-180 per adult per month for basic insurance

Premiums vary by insurer, policy type and voluntary excess. Supplementary packages add cost.

Liability insurance

Often around EUR 3-8 per month

Family policies usually cost more than single-person policies. Limits and exclusions matter.

Contents insurance

Often around EUR 5-20 per month

Cost depends on postcode, insured value, building type, security and selected add-ons.

Travel insurance

Often around EUR 3-15 per month for continuous cover

Worldwide cover, cancellation, winter sports and business travel can change the premium.

Insurance directory

Use this page to compare providers, learn coverage basics and understand Dutch insurance requirements before requesting quotes or speaking with an insurer.

Dutch basic health insurance is generally mandatory if you live or work in the Netherlands. Timing and exceptions depend on your situation, so check Government.nl, Zorginstituut Nederland and the insurer before relying on home-country cover.

Health insurance is the major requirement for most residents and workers. Car liability insurance is required if you own and use a car. Other products, such as personal liability, contents and travel insurance, are usually optional but commonly compared.

Contents insurance is usually optional for renters, but many tenants choose it to cover belongings under policy conditions. Check what the landlord or furnished-apartment provider covers before buying.

Yes. Personal liability insurance is common in Dutch households because it can cover certain everyday liability situations. It is not a substitute for business liability or professional liability cover.

Many large Dutch insurers support online onboarding and some English-language information, but English service levels vary. Compare providers such as Zilveren Kruis, VGZ, CZ, FBTO, Nationale-Nederlanden, a.s.r., Univé, OHRA, Allianz and Aon based on your specific product needs.

Homeowners commonly compare building insurance, contents insurance, liability insurance and sometimes life insurance linked to mortgage planning. Mortgage lenders or owners' associations may influence what is required.

ZZP'ers often compare business liability, professional liability, equipment insurance and income protection. Requirements can depend on clients, contracts, sector rules and personal risk tolerance.

Most major Dutch insurers offer online portals or apps, but the level of English support, document upload, claims handling and cancellation controls varies by provider and product.

Insurance products, premiums and regulations can change over time. Always verify current information with providers and official resources.

Health insurance requirements, official government information and public-service guidance

Open sourceDutch healthcare insurance system, basic package context and public healthcare information

Open sourceFinancial markets supervision, consumer information and provider-checking context

Open sourceEntrepreneur and business-insurance context for companies and self-employed people

Open source