Unfamiliar Dutch systems

Pension funds, AOW, Box 1/2/3 and buyer costs (k.k.) use terminology and rules that may differ sharply from your home country.

Netherlands · Services · Financial advisors

Find trusted financial advisors who help expats and international professionals navigate pensions, investments, taxes, wealth planning and long-term financial decisions in the Netherlands.

Provider inclusion is informational, not a recommendation. This page is not investment, tax or retirement advice — verify AFM credentials, fees and scope directly with providers.

Overview

Many expats seek financial advice when Dutch pension statements, Box 3 reporting, mortgage capacity and long-term savings targets feel unfamiliar — especially after a mid-year move or when assets remain in another country.

A financial advisor may help translate your household goals into a structured plan: pension gaps, investment horizon, property affordability, emergency reserves and what happens if you leave the Netherlands again.

This directory is not investment, tax or retirement advice and does not rank providers. Use it to understand advisor models, compare real firms and prepare better questions before sharing sensitive financial information.

Pension funds, AOW, Box 1/2/3 and buyer costs (k.k.) use terminology and rules that may differ sharply from your home country.

Arrival date, contract type and a possible departure within a few years can reset priorities for property, pensions and savings.

Overseas pensions, foreign investments, rental property and multi-currency income often need coordinated planning — not isolated decisions.

Buying property, investing a bonus, pre-retirement reviews or inheritance planning benefit from a written household view before you act.

At a glance

Practical orientation points before comparing providers or booking consultation calls.

Planning scope

Long-term

Pensions, savings, investments, property timing and major life transitions — not day-to-day tax filing.

Expat relevance

Common

Internationally mobile professionals often need cross-border pension, asset and relocation planning.

Typical fees

Varies

Fixed planning packages, hourly rates or asset-based fees — confirm scope and payment timing in writing.

Regulation

AFM context

Investment advice and certain wealth services fall under Dutch financial supervision — verify credentials.

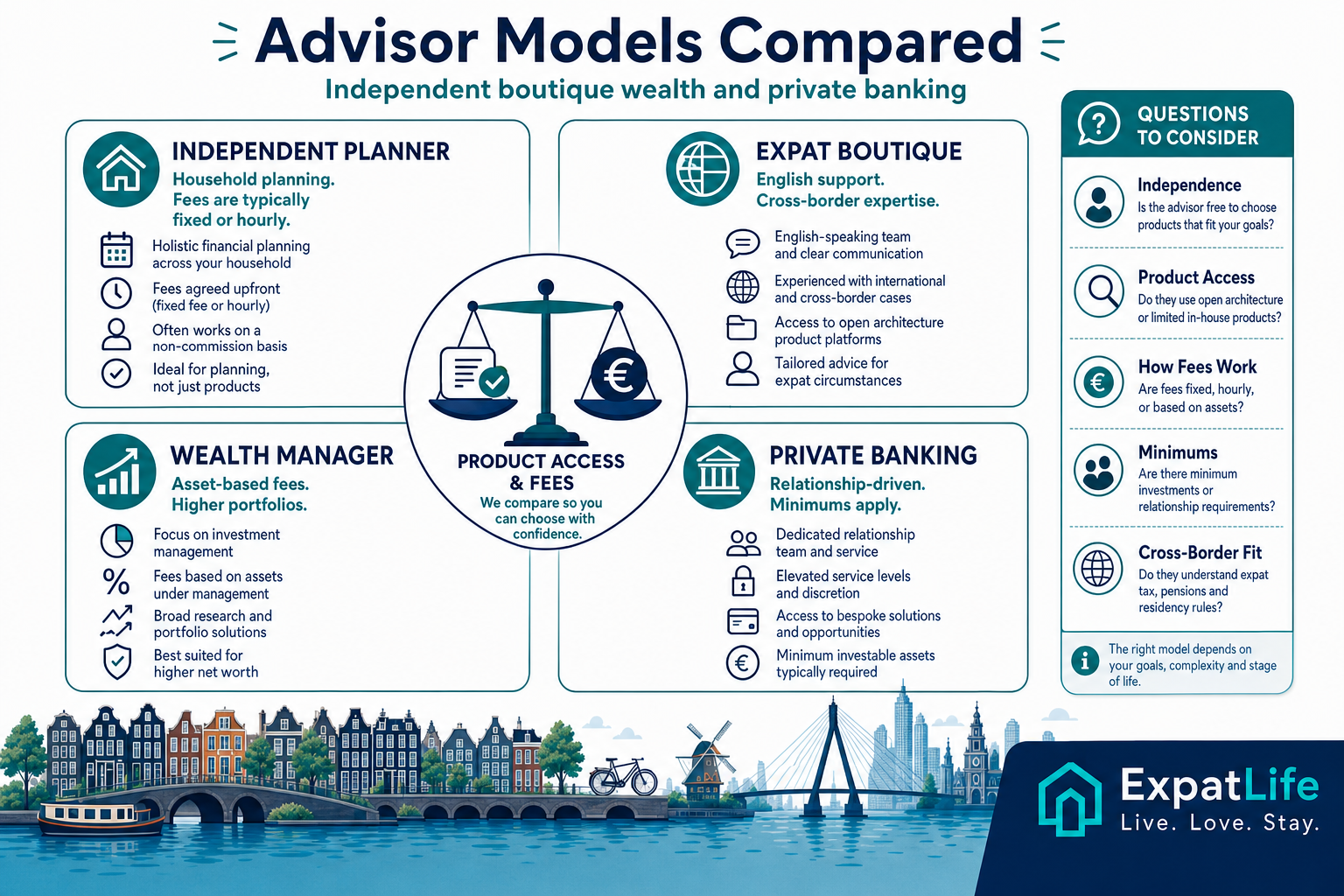

Advisor models

Multiple types

Independent planners, expat boutiques, wealth managers and private banking serve different profiles.

Guarantee

None

No advisor can guarantee investment returns, pension outcomes or tax results.

Advisor role

Scope varies by provider — some offer planning-only conversations, others also implement investments or refer tax and legal specialists. Confirm inclusions before you engage.

Project pension gaps using employer statements, AOW estimates and private savings targets — often with scenario modelling for different retirement ages.

Discuss risk tolerance, time horizon and portfolio structure. Confirm whether advice includes product selection or planning-only guidance.

Align plans with relocation timing, contract type, residence status and whether you may leave the Netherlands before retirement.

Map net income against fixed costs (rent, insurance, childcare), emergency reserves and monthly savings capacity.

Explain Dutch pension building blocks and how they interact with overseas pensions — outcomes still depend on fund rules and personal history.

Plan around arrival or departure: when to move assets, adjust savings rates or delay major purchases like property.

Coordinate assets, pensions and income across countries — often alongside tax advisors for reporting and treaty context.

High-level review of beneficiaries, wills and cross-border estate complexity — legal drafting usually sits with notaries or lawyers.

| Profile | What can matter | Example question |

|---|---|---|

| Highly skilled migrant, first 2 years in NL | 30% ruling, employer pension accrual, emergency fund, property vs rent horizon. | Should I maximise pension contributions now or keep liquidity for a possible move? |

| Dual-income household with children | Childcare costs, school fees, housing space, insurance and long-term savings targets. | How much should we reserve monthly after fixed costs and pension contributions? |

| Remote worker with foreign employer | Income currency, cross-border tax context, pension gaps and investment platform choice. | Can my current investment accounts stay open while I am Dutch-resident? |

| Pre-retirement expat in NL | AOW accrual, employer pension payout options, overseas assets and healthcare cost planning. | What income mix should I expect from AOW, employer pension and private savings? |

Advisor models

Different models compare different product sets, fee structures and minimum client profiles. Match the model to your assets, complexity and language needs.

May offer broad planning advice with transparent fee models and varying product access.

Useful when: You want a planning-first conversation about pensions, savings, investments and major life goals.

Often positions around English-language support and internationally mobile client files.

Useful when: Your planning questions involve relocation, foreign income, overseas pensions or cross-border complexity.

Typically serves higher-asset clients with integrated banking, investment and advisory services.

Useful when: You need institutional-grade wealth management and may already meet asset thresholds.

| Item | Typical range | What to confirm |

|---|---|---|

| Introductory consultation | Often free to paid | Whether the first meeting is no-obligation and what documents you should bring. |

| Financial plan package | Provider-specific fixed fee | Whether pensions, investments, property and cross-border topics are all included. |

| Ongoing advisory relationship | Annual or asset-based | Review frequency, investment monitoring scope and what triggers extra charges. |

| Investment implementation | Separate from planning | Whether product fees, platform costs and custody charges sit on top of advice fees. |

Dutch context

Dutch pensions, tax boxes, housing costs and insurance premiums shape monthly cash flow differently from many home countries — planning should reflect local rules and your stay horizon.

Employer schemes (often via pension funds), AOW state pension and private savings may all appear on one household plan — accrual rules differ if you arrived mid-career.

Residency, Box 1/2/3 context and the 30% ruling can change how planning assumptions should be framed — tax filing itself is usually a separate service.

Rent versus buy, mortgage capacity, buyer costs (k.k.) and mobility plans should sit in the same cash-flow conversation.

Toeslagen and childcare benefit eligibility can affect monthly budgets — verify official rules rather than relying on informal estimates.

Mandatory basisverzekering plus optional aanvullende verzekering are fixed monthly costs that affect disposable income.

Emergency funds (often 3–6 months of fixed costs), investment accounts and pension gaps are commonly reviewed together.

| Budget line | Example figure | Why it matters in planning |

|---|---|---|

| Net household income | €5,800/month after tax | Confirm whether figures assume 30% ruling, partner income and bonus timing. |

| Fixed housing | €1,950 rent or €2,100 mortgage | Include VvE, OZB, insurance and maintenance reserves if you own. |

| Health insurance | €135 basis + €45 aanvullend | Mandatory monthly cost that reduces investable surplus. |

| Pension contributions | Employer + employee via salary | Check pension portal projection, not payslip line alone. |

| Investable surplus | €600–€900/month target | Split between emergency fund, pension gap and long-term investments. |

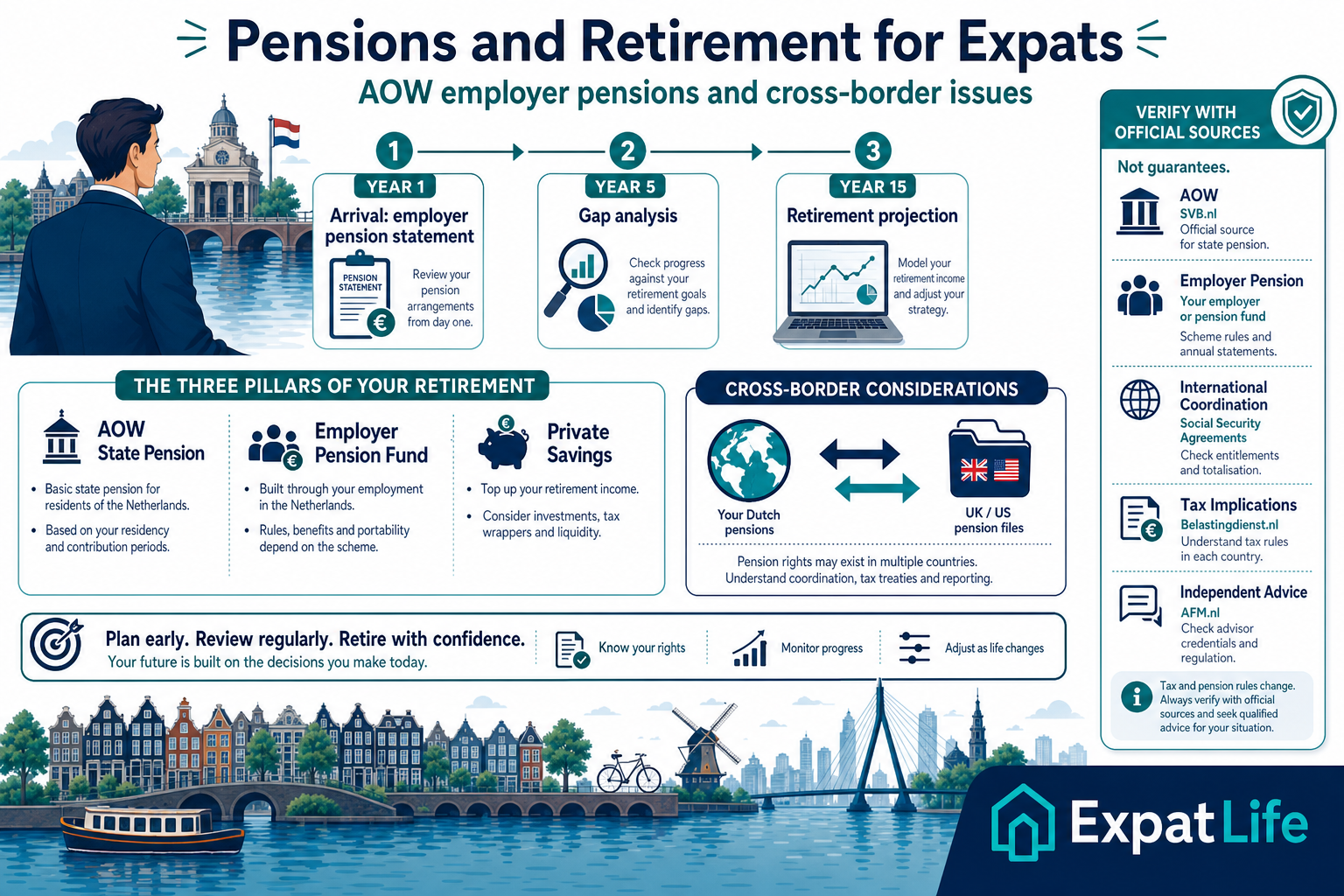

Pensions

Employer schemes, AOW and private savings are often reviewed together. This section is informational — not pension advice. See our pension guide for deeper context.

Many employees accrue rights through employer schemes — check jaaropgave, pension portal projections and what happens if you leave before retirement age.

AOW accrual depends on years resident in the Netherlands — late arrivals may receive a reduced entitlement unless topped up.

Some households supplement employer and state pensions with investments or annuities — suitability depends on horizon and risk tolerance.

UK, US, EU or other overseas pensions may have transfer restrictions, currency risk and tax treatment that need specialist review.

| Profile | Scenario | Planning question | Useful record |

|---|---|---|---|

| Arrived in NL at age 35 | 15 years of AOW accrual possible before age 67 if resident throughout | How does a partial AOW affect my target retirement income? | SVB AOW estimate, employer pension projection |

| Employer pension + UK workplace pension | Two pension pots in different currencies and regulatory systems | Should I consolidate, leave separate or adjust savings rate? | Both pension statements, transfer rules summary |

| Temporary contract, uncertain stay | Limited employer pension accrual and possible departure within 4 years | How much should I save privately if employer accrual is low? | Contract end date, pension fund rules, current savings rate |

Investing

This page does not recommend investments. Use this section to understand discussion topics, then confirm regulatory scope, fees and independence with any advisor.

Some expats keep home-country brokerage accounts; others open Dutch or EU platforms — residency, reporting and platform terms differ.

Multi-currency portfolios may need coordination with tax residency, estate planning and future repatriation plans.

Box 3, foreign withholding and home-country reporting can affect net returns — planning context is not the same as tax advice.

Retirement, property purchase, education funding or business exit each imply different risk, liquidity and time horizons.

| Profile | Example figure | Issue to check | Useful record |

|---|---|---|---|

| First-time investor in NL | €500/month surplus after costs | Emergency fund size, platform choice, risk profile and whether advice includes implementation | Bank statements, fixed cost overview, existing debts |

| Existing portfolio abroad | €120,000 in US/UK accounts | Whether accounts remain accessible, reporting obligations and currency exposure | Broker year-end statements, account terms, residency date |

| Windfall or bonus planning | €40,000 bonus after tax | Liquidity needs, pension gap, property timing and whether lump-sum investing fits risk tolerance | Payslip, bonus letter, current asset allocation |

Property

Property timing should reflect relocation horizon and cash reserves, not just mortgage capacity. Connect with our mortgage advisors directory and buying guide for housing-specific steps.

Advisors may help test whether buying fits your relocation horizon, emergency reserves and monthly cash-flow buffer.

Monthly payments, interest deductibility context (for owner-occupiers) and buyer costs affect how much you can save or invest elsewhere.

Maintenance, VvE charges, insurance, municipal taxes (OZB) and mobility plans belong in the same household model.

Temporary contracts or a likely departure within 3–5 years can make renting or delaying purchase the more flexible option.

| Profile | Scenario | Planning question | Useful record |

|---|---|---|---|

| HS migrant, 3-year contract | Renting €1,850/month, considering €450k purchase | Does buying fit if I may leave in year 3? | Contract end date, mortgage quote, buyer cost estimate |

| Dual income, planning to stay | €520k target home, €2,050/month mortgage estimate | Can we keep investing €800/month after buying? | Mortgage capacity letter, fixed cost overview, emergency fund balance |

| Owner abroad, renting in NL | UK rental income + NL salary | How does foreign property affect NL cash-flow planning? | Foreign mortgage statement, rental summary, NL net income |

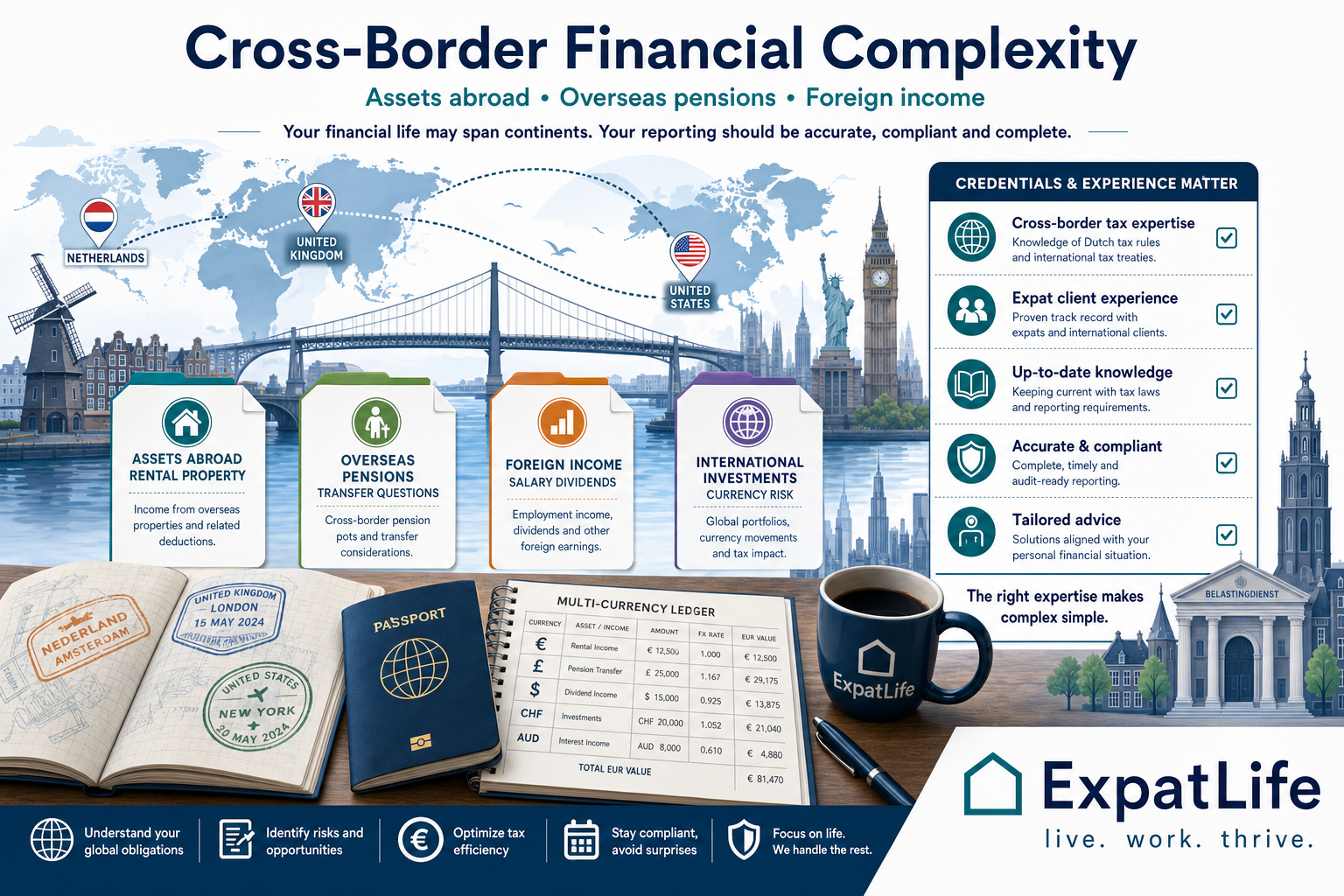

Cross-border

List every country where you hold income, pensions or assets before shortlisting advisors. Cross-border files often need both planning and tax specialist support.

Property, investments and bank accounts in other countries may need coordinated reporting, currency planning and estate considerations.

Pension rights from previous countries may affect retirement projections, payout timing and tax treatment in the Netherlands.

Salary, dividends or rental income from outside the Netherlands can shape cash flow and may overlap with tax advisor work.

Cross-border platforms, US-person rules and treaty context can make investment structure more sensitive for mobile residents.

| Profile | Example concern | Practical move |

|---|---|---|

| US citizen resident in NL | US filing obligations plus Dutch residency and investment reporting | Confirm whether the advisor coordinates with US-specialist tax support or refers out. |

| Rental property in home country | Foreign rental cash flow, mortgage and Dutch reporting context | Bring lease, local tax return and annual mortgage statement to planning calls. |

| Planning to leave NL in 3 years | Pension preservation, property sale timing and investment account portability | Ask how the advisor models departure scenarios and what triggers a plan review. |

Common challenges

Use these cards to identify where your situation may need specialist support — then ask advisors directly about relevant experience.

Employer schemes, AOW and private savings use terminology (e.g. franchise, uitkering) that may feel unfamiliar without a walkthrough.

A move to or from the Netherlands can reset assumptions about retirement age, tax residency and where assets should sit.

Becoming or ceasing to be a Dutch tax resident can change reporting, allowances and which planning priorities matter first.

Home-country accounts and platforms may have different accessibility, fees and reporting expectations once you live in NL.

Some expats own property in multiple countries, which adds cash-flow, currency and estate complexity to one household plan.

Unclear departure dates make it harder to judge pension gaps, savings targets and whether illiquid investments are appropriate.

Income, assets and future expenses may sit in EUR, GBP, USD or other currencies with exchange-rate risk.

Frequent moves can make long-term planning feel provisional — advisors may help structure flexible milestones instead of fixed assumptions.

Avoidable mistakes

Financial planning and Dutch tax compliance are related but different — confirm who handles each part.

Product-linked advice, asset-based fees and referral commissions can affect recommendations.

English-language websites are helpful, but credentials, licenses and case experience still need verification.

Use an introductory call to confirm services, fees and confidentiality before uploading sensitive documents.

If you may leave the Netherlands, plans built only for permanent residency can misallocate savings or property timing.

Neutral listings are not rankings — compare scope, languages, fees and fit for your file.

When to consider advice

| Situation | Numbers to bring | Documents to bring |

|---|---|---|

| New expat, first planning call | Monthly net income, fixed costs, current savings, pension contribution rate | Contract, recent payslips, bank statements, BSN registration date |

| Cross-border household | Assets by country, pension values, foreign rental income, planned departure window | Pension statements abroad, property summaries, latest tax residency evidence |

| Pre-retirement review | Target retirement age, desired monthly income, current pension projections | Employer pension portal export, AOW estimate, investment account statements |

City coverage

Many advisors work online nationwide — compare both city experience and digital process quality.

Directory

This structured directory uses real companies and neutral descriptions. It does not rank providers or guarantee outcomes.

Amsterdam

Financial planning firm focused on internationally mobile professionals and expatriates in Europe.

Expat focus

Public materials emphasise expat financial planning, cross-border complexity and English-language advisory support.

Focus areas

Expat planning · Retirement · Investments · Cross-border

Amsterdam

Wealth management and financial planning organisation serving international clients in the Netherlands.

Expat focus

Positions around wealth management and financial planning for internationally oriented households.

Focus areas

Wealth management · Investments · Retirement · Financial planning

Amsterdam

Independent financial advice provider offering planning support for residents in the Netherlands.

Expat focus

May be relevant for expats seeking independent planning conversations in English or Dutch.

Focus areas

Financial planning · Pensions · Investments · Insurance context

Netherlands

Wealth planning organisation offering structured financial planning for households in the Netherlands.

Expat focus

Public pages include English-language wealth planning information for internationally oriented clients.

Focus areas

Wealth planning · Retirement · Investments · Estate discussions

Amsterdam

Private banking and wealth management group serving affluent households and entrepreneurs.

Expat focus

International private banking and wealth management; may suit higher-asset internationally mobile clients.

Focus areas

Private banking · Wealth management · Investments · Estate planning context

Amsterdam

Wealth management brand offering private banking and investment services in the Netherlands.

Expat focus

May be relevant for affluent expats seeking integrated wealth management; English support varies by team.

Focus areas

Wealth management · Investments · Private banking

Amsterdam

Wealth management firm serving international professionals and entrepreneurs.

Expat focus

Public positioning includes support for internationally mobile clients and English-language services.

Focus areas

Wealth management · Investments · Financial planning · Cross-border

Netherlands

Advisory service oriented toward expats seeking investment and financial planning guidance in the Netherlands.

Expat focus

Dedicated expat positioning around investment discussions and financial planning for internationals.

Focus areas

Investments · Expat planning · Retirement context

The Hague

Financial planning practice supporting internationally oriented households in the Netherlands.

Expat focus

Positions around expat-friendly financial planning and long-term household planning.

Focus areas

Financial planning · Retirement · Budgeting · Expat planning

Netherlands

Professional association network of financial planners in the Netherlands; useful for finding certified planners.

Expat focus

Directory-style network rather than a single firm; English-speaking members may vary by region.

Focus areas

Financial planning · Pensions · Investments · Insurance context

Comparison table

Use this as a starting point for your shortlist — verify all details directly with each provider.

| Advisor | Cities Served | Expat Focus | Languages | Online | Focus Areas |

|---|---|---|---|---|---|

| Black Swan Capital Europe | Amsterdam, Netherlands-wide | Dedicated expat focus | English | Yes | Expat planning, retirement, investments, cross-border |

| Octas Capital | Amsterdam, Netherlands-wide | International clients | English, Dutch | Yes | Wealth management, investments, retirement |

| Holland Financial Centre | Amsterdam, Netherlands-wide | Expat-friendly planning | English, Dutch | Yes | Financial planning, pensions, investments |

| VWP Wealth Planning | Netherlands-wide, online | International positioning | English, Dutch | Yes | Wealth planning, retirement, investments |

| FINEX Wealth Management | Amsterdam, international | International professionals | English, Dutch | Yes | Wealth management, investments, cross-border |

| Expat Investment Advice | Netherlands-wide, online | Dedicated expat focus | English | Yes | Investments, expat planning, retirement context |

| Blue Horizon Financial Planning | The Hague, Randstad, online | Expat-friendly boutique | English, Dutch | Yes | Financial planning, retirement, budgeting |

| Van Lanschot Kempen | Amsterdam, multiple cities | International private banking | English, Dutch | Yes | Private banking, wealth management |

Provider support

Use these contact options after comparing the directory — financial planners and wealth managers first, then complementary banking and cross-border support where relevant. Verify scope, credentials and fees before sharing sensitive information.

These providers can help users move from research to a real financial planning conversation: expat-focused planners, wealth managers, cross-border support and banking pathways. Treat this as a discovery list, not a ranking or recommendation.

Some links may be affiliate or referral links. If you use them, we may earn a commission at no extra cost to you. Ordering reflects relevance to expat financial-advisor discovery, not pay-to-rank placement. This is not investment, tax, pension or financial advice; verify AFM registration where relevant and confirm fees, scope, credentials and terms directly with licensed advisers and providers. Learn more

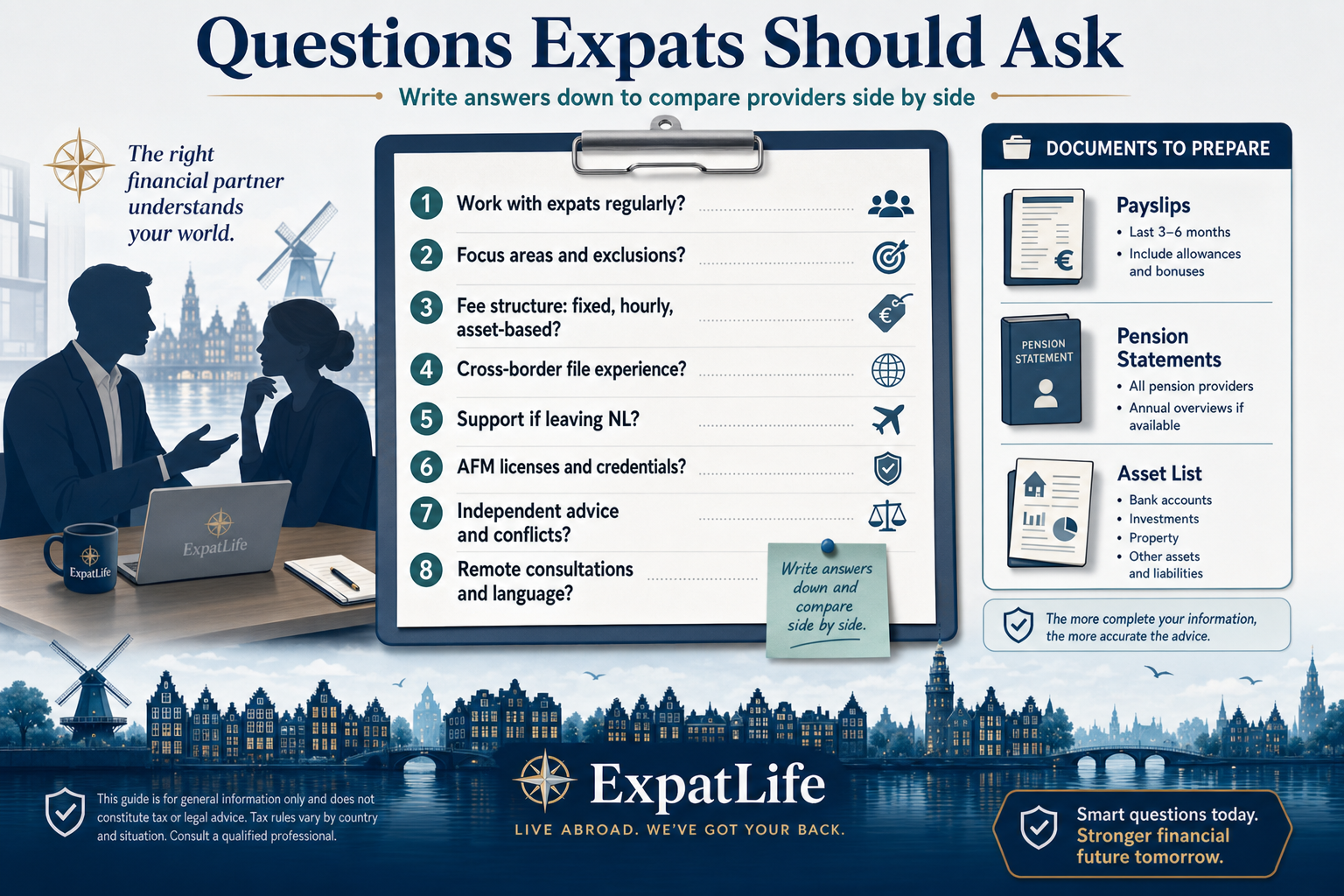

Advisor interview

Strong answers reveal independence, fee structure, cross-border experience and regulatory credentials. Write responses down to compare providers side by side.

| Document | Why it matters |

|---|---|

| Recent payslips and employment contract | Shows income stability, contract type and whether planning should assume a fixed departure date. |

| Pension statements (NL and abroad) | Employer scheme projections, AOW context and overseas pension rights shape retirement planning. |

| Asset and account summaries | Bank balances, investments, property equity and debts define starting net worth and liquidity. |

| Mortgage or rent overview | Housing costs and buyer plans affect cash flow and long-term affordability. |

| Tax residency and 30% ruling context | Planning assumptions may differ for new arrivals, ruling holders and people with foreign income. |

| Relocation timeline | Arrival date, expected departure and family plans change whether property, pensions or investments should be prioritised. |

Financial guides

Financial planning connects to tax, pension, housing and cross-border income — read these guides to arrive at advisor calls with clearer questions.

Provider discovery

Use the directory to compare provider scope, city coverage, language support and focus areas. Then request an introduction or contact shortlisted advisors directly to verify fees, credentials and fit.

Before you book

FAQ

Use these FAQ answers to identify what you still need to verify: advisor scope, fee structure, cross-border experience, regulation and whether your expat file needs specialist support.

Not every expat needs one. Many seek support when Dutch pension statements feel unclear, finances span countries or a major decision (property, retirement, inheritance) needs structure. Start with free official pension information and our guides; use an advisor when complexity or confidence gaps remain.

Typical topics include retirement projections, investment structure, budgeting, pension explanations, relocation transitions and cross-border wealth coordination. Scope varies — some firms plan only, others also implement investments. Confirm inclusions before engaging.

Some specialise in multi-country files with overseas pensions, property and investment accounts. Others focus on Dutch-resident households only. Ask for examples of similar client profiles and which topics they refer to tax or legal specialists.

Many explain employer pension statements, AOW context and private savings gaps. They do not replace pension funds or guarantee payout amounts. Bring your pension portal export and ask what assumptions the advisor uses in projections.

Yes — common topics include 30% ruling context in planning (not filing), contract stability, property timing and building emergency reserves after relocation. Ask whether the advisor regularly works with your nationality and employment pattern.

Models include fixed planning packages, hourly rates, annual retainers and asset-based percentages. Confirm what triggers extra fees, whether investment products add separate charges and when payment is due. Request a written quote before sharing full financial details.

Most providers offer video or phone meetings and secure document upload. Confirm language support, time zones, data handling and whether complex topics still benefit from in-person sessions.

Check AFM registers for investment advice and relevant Wft permissions, read advisory agreements carefully and confirm DNB context for private-banking relationships. Directory inclusion here is not a credential check — verify directly.

Trust

Official sources help you verify regulatory context. Confirm credentials, licenses and advisory agreements directly with each provider before engaging.

Related guides

Use these guides to connect the provider decision to tax, pension, housing and city context.

Services ecosystem

Financial advice is one part of a wider money and relocation ecosystem — choose the professional that matches your immediate question.

Explore next

Move from provider discovery into mortgage, pension, tax and property guides that shape long-term financial decisions.